Jennifer Dochstader04.06.06

In the fall of 2003 I attended the Tag and Label Manufacturers Institute (TLMI) Technical Seminar in Chicago. Joining in discussions with label converters during the coffee breaks between presentations, it was clear which subject was at the forefront of the industry's collective consciousness: mandated pricing declines. Consumer packaged goods companies (CPGs) were enforcing annual incremental pricing decreases with their label vendors.

One converter's tongue-in-cheek comment captured the sentiment of much of the industry at the time: "I have customers who are telling me that if I want to continue to be one of their suppliers I have to drop my prices by 10 percent a year. I said to these clients, 'So that means in 10 years my labels are going to be free?' "

Present day business conditions remain much the same. A quick perusal of quarterly earnings reports for Fortune 500 CPGs is an exercise in repetition: Companies like Procter & Gamble, Cadbury Schweppes, Nestlé, and Danone continue to be slammed by commodity pricing increases as what these companies pay for everything from packaging resins to oil to coffee beans continues to rise. Added to this equation is the continued pressure these companies face from the major retailers and the threat of private labeled product growth. The name of the game undoubtedly will continue to be imposed cost declines landing further on down the supply chain right into the label converter's lap. Or will it?

Label converters have been squeezed from both ends of the supply chain. While their customers have been mandating price declines, their material suppliers have been simultaneously raising prices in response to escalating raw material costs.

One of the central issues our industry presently faces is whether price declines will continue or stabilize, or whether prices will actually begin to increase. Interestingly, the industry — both at the converter and print buyer level — appears divided on this issue.

LPC Inc., an industry research and strategic marketing firm, has been closely tracking pricing trends in the packaging industry for the past three years. We have been periodically polling package printers and print buyers across end-use categories to ascertain average mandated pricing declines in the label, flexible packaging and folding carton sectors.

In the first quarter of 2006, LPC polled packaging procurement personnel at more than 100 consumer packaged goods companies. These persons are either directly involved in, or oversee the procurement of, pressure sensitive, cut and stack, non-PS, and/or shrink labels.

CPGs were asked to quantify mandated average price declines that were enforced upon their label vendors in 2005. As the graph illustrates, 86 percent of polled consumer package goods companies indicated that they enforced mandated price declines of one to 10 percent with their label vendors in 2005. In discussions with procurement personnel, the impetus behind these decreases is a predictable formula of cause and effect: rising commodity prices eroding CPG margins, pressure from the major retailers, and the constant objective of trying to lower costs in the supply chain.

Label converters remain acutely aware of CPG cost-cutting initiatives, as they've witnessed their own margins impacted by their customers' mandates. As with the CPG universe, LPC recently polled more than 100 converters located throughout the United States and Canada in order to garner feedback from the converters' own perspective. Converters were asked to quantify the price decline mandates imposed by their customers in 2005.

As this chart illustrates, there isn't a significant discrepancy between the discounted amounts label procurement personnel indicate they paid, and the price declines converters reported enduring, in 2005. While companies in both the CPG and converting universes seem to agree on historical pricing data, it's the future where folks diverge.

Our research indicates that 2006 may be a pivotal year for industry pricing trends. Both polled consumer package goods companies and label converters were asked what their pricing trend projections were for 2006 and 2007 and the responses from both groups reveals a positive shift for suppliers.

Just over half of those consumer package goods companies we polled indicated that they anticipate the prices they pay for labels to actually increase this year. These respondents represented all end-use categories and shared a similar reasoning process behind these anticipated price rises. Procurement personnel from companies like Coors, Clorox and Colgate Palmolive emphasized how important innovation was in regards to their label suppliers. "Our packaging suppliers have to be able to invest back into their businesses," commented a sourcing manager. "We continuously depend on the high levels of innovation that come from our vendors." McCain Foods and Sara Lee stressed the importance of partnerships, and that continued mandated pricing declines can deteriorate the partnership into a lose-lose. While Procter & Gamble and Kraft stressed the cost associated with qualifying new vendors, a process that can take anywhere from four to eight months.

Asked what they predict pricing trends will be for 2006 and into 2007, the majority of label converters are optimistic. Label converters across revenue ranges are anticipating prices will rise in the coming year. Asked what the primary factors are that will drive these increases, converters cite a host of reasons including a reinforced commitment to the converter-CPG partnership; to passing along their own raw material increases; to being willing to potentially walk away from an account when a client threatens to put a piece of business out to bid if certain price mandates aren't met.

Faced with mandated price declines over the past half decade, label converters have had to either take direct hits to their own margins, ascertain ways to take additional costs out of the production process, or convince their customers that the value added services they provide are worth paying extra for. While it appears that pricing trends won't go in a favorable direction for every label converter, the majority seem ready for some long-overdue validation.

One converter's tongue-in-cheek comment captured the sentiment of much of the industry at the time: "I have customers who are telling me that if I want to continue to be one of their suppliers I have to drop my prices by 10 percent a year. I said to these clients, 'So that means in 10 years my labels are going to be free?' "

Present day business conditions remain much the same. A quick perusal of quarterly earnings reports for Fortune 500 CPGs is an exercise in repetition: Companies like Procter & Gamble, Cadbury Schweppes, Nestlé, and Danone continue to be slammed by commodity pricing increases as what these companies pay for everything from packaging resins to oil to coffee beans continues to rise. Added to this equation is the continued pressure these companies face from the major retailers and the threat of private labeled product growth. The name of the game undoubtedly will continue to be imposed cost declines landing further on down the supply chain right into the label converter's lap. Or will it?

Label converters have been squeezed from both ends of the supply chain. While their customers have been mandating price declines, their material suppliers have been simultaneously raising prices in response to escalating raw material costs.

One of the central issues our industry presently faces is whether price declines will continue or stabilize, or whether prices will actually begin to increase. Interestingly, the industry — both at the converter and print buyer level — appears divided on this issue.

LPC Inc., an industry research and strategic marketing firm, has been closely tracking pricing trends in the packaging industry for the past three years. We have been periodically polling package printers and print buyers across end-use categories to ascertain average mandated pricing declines in the label, flexible packaging and folding carton sectors.

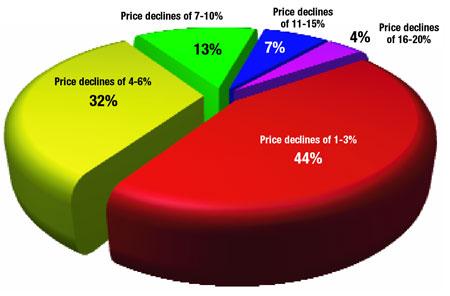

According to CPGs: Mandated price declines for 2005

In the first quarter of 2006, LPC polled packaging procurement personnel at more than 100 consumer packaged goods companies. These persons are either directly involved in, or oversee the procurement of, pressure sensitive, cut and stack, non-PS, and/or shrink labels.

CPGs were asked to quantify mandated average price declines that were enforced upon their label vendors in 2005. As the graph illustrates, 86 percent of polled consumer package goods companies indicated that they enforced mandated price declines of one to 10 percent with their label vendors in 2005. In discussions with procurement personnel, the impetus behind these decreases is a predictable formula of cause and effect: rising commodity prices eroding CPG margins, pressure from the major retailers, and the constant objective of trying to lower costs in the supply chain.

According to converters: Mandated price declines for 2005

Label converters remain acutely aware of CPG cost-cutting initiatives, as they've witnessed their own margins impacted by their customers' mandates. As with the CPG universe, LPC recently polled more than 100 converters located throughout the United States and Canada in order to garner feedback from the converters' own perspective. Converters were asked to quantify the price decline mandates imposed by their customers in 2005.

As this chart illustrates, there isn't a significant discrepancy between the discounted amounts label procurement personnel indicate they paid, and the price declines converters reported enduring, in 2005. While companies in both the CPG and converting universes seem to agree on historical pricing data, it's the future where folks diverge.

According to CPGs: Projected label pricing trends for 2006-2007

Our research indicates that 2006 may be a pivotal year for industry pricing trends. Both polled consumer package goods companies and label converters were asked what their pricing trend projections were for 2006 and 2007 and the responses from both groups reveals a positive shift for suppliers.

Just over half of those consumer package goods companies we polled indicated that they anticipate the prices they pay for labels to actually increase this year. These respondents represented all end-use categories and shared a similar reasoning process behind these anticipated price rises. Procurement personnel from companies like Coors, Clorox and Colgate Palmolive emphasized how important innovation was in regards to their label suppliers. "Our packaging suppliers have to be able to invest back into their businesses," commented a sourcing manager. "We continuously depend on the high levels of innovation that come from our vendors." McCain Foods and Sara Lee stressed the importance of partnerships, and that continued mandated pricing declines can deteriorate the partnership into a lose-lose. While Procter & Gamble and Kraft stressed the cost associated with qualifying new vendors, a process that can take anywhere from four to eight months.

According to converters: Projected pricing trends for 2006-2007

Asked what they predict pricing trends will be for 2006 and into 2007, the majority of label converters are optimistic. Label converters across revenue ranges are anticipating prices will rise in the coming year. Asked what the primary factors are that will drive these increases, converters cite a host of reasons including a reinforced commitment to the converter-CPG partnership; to passing along their own raw material increases; to being willing to potentially walk away from an account when a client threatens to put a piece of business out to bid if certain price mandates aren't met.

Faced with mandated price declines over the past half decade, label converters have had to either take direct hits to their own margins, ascertain ways to take additional costs out of the production process, or convince their customers that the value added services they provide are worth paying extra for. While it appears that pricing trends won't go in a favorable direction for every label converter, the majority seem ready for some long-overdue validation.