Jennifer Dochstader08.25.06

Over the past three years the North American label printing industry has witnessed an unprecedented rise in acquisition activity. The ownership of companies across revenue ranges is increasingly changing hands — some acquired by strategic investors (printing and packaging conglomerates) and some by financial investors (private equity firms and financial services companies). The evolutionary foundation upon which our industry was built is shifting as the entrepreneurs who founded companies in the 1960s, '70s and '80s are approaching retirement age in a market where private equity capital has never been so plentiful, nor valuations so high. This article explores some of the options available to label company owners today, in the hope of providing assistance as they navigate the complex waters of acquisition and the positioning process.

For many owners, it's hard even to begin contemplating the notion of selling. Many of these industry pioneers have been at the forefront of innovation and, press by press, square foot by square foot, they have grown their companies into the successful manufacturing profit centers they are today. Other owners, however, take a different, more circumspect view. They've seen the decades of booming growth come and go and as raw material prices continue to escalate and cost-cutting pressure from their customers continues to rise (while label vendor loyalty seemingly plummets), these owners are ready to take a hard look at their options, understanding that there has been no better time to position a label company for sale.

For many owners, it's hard even to begin contemplating the notion of selling. Many of these industry pioneers have been at the forefront of innovation and, press by press, square foot by square foot, they have grown their companies into the successful manufacturing profit centers they are today. Other owners, however, take a different, more circumspect view. They've seen the decades of booming growth come and go and as raw material prices continue to escalate and cost-cutting pressure from their customers continues to rise (while label vendor loyalty seemingly plummets), these owners are ready to take a hard look at their options, understanding that there has been no better time to position a label company for sale.

One of the primary forces at work in creating the current "seller's market" scenario is the flood of private equity capital available today to invest in privately held businesses. John-Michael Girald, principal of the Bigelow Company, a New Hampshire, USA based private investment bank that has worked with label printing companies, comments on today's private equity landscape. "In our database alone we have more than 1,000 private equity firms who have each raised more than $100 million in private equity capital. If you do the math, that's around $100 billion worth of purchasing power out there today and they're investing in private companies across the country. It's a unique situation for the private company owner, because all of a sudden they have a multitude of entities wanting to bid on their business, and it is driving prices up."

Why the present private equity frenzy? Analysts claim that there are a host of explanations for this, and Girald attributes it to several key factors pervading the marketplace. "Everyone has asset allocation for their own portfolios," Girald continues, "and as the Sarbanes-Oxley Act has imposed strict accounting rules onto public companies, it makes less and less sense for small public companies to actually be public. As part of everyone's asset allocation they always invest a percentage of their money in small cap stocks, and as these stocks go away due to forces like Sarbanes-Oxley, to satisfy these small company portfolio requirements they're looking to private equity which invests in small companies in a liquid market." The graph on this page illustrates uninvested private equity capital growth over the course of the past decade.

For many label company owners, the world of private equity is an unknown. Historically, an owner considering the sale process might sit down with one of the known acquiring "strategics" — a CCL, a WS Packaging, or a Clondalkin, for example. Said owner might think his or her company is a good fit for one of these conglomerates given the company's application mix, or technology base. Some owners still view this as their best bet scenario.

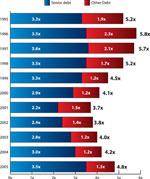

Girald believes, however, that this approach is often not in the owner's best interest. "In our view, the strategic investors have their own opinion of the industry, and what we found is that the strategics often had a lower opinion of the value of a business than the private equity firms. You might get a strategic coming in with a valuation of four to five times [four to five times EBITDA] even though a company warrants a higher valuation. No matter how you try pitching this company to a group of strategics, they have a set valuation for what they pay for companies because they believe their industry experience justifies that number." The graph at right illustrates debt multiples over the course of the past decade.

Strategic investors might not want to generally boost valuation offerings, but there are some situations where a label company might be uniquely positioned to deliver its own differentiating value proposition — with RFID, for example — and in this situation a strategic investor might be willing to pay beyond the limits of the private equity universe.

Both strategic and private equity investors can deliver a scenario that is in alignment with the desires of the private company owner. Burgaw, NC, USA based Prestige Label was recently sold to Atlantic Packaging, a family owned company active in commercial and customized paper and paperboard converting. Elisha Tropper, the former president of Prestige Label, comments on his company's journey in the acquisition process.

"A priority for us was to make sure that whoever bought the company was going to keep the company in its current location and retain the employees. Atlantic was the perfect buyer. They're a large company with eight locations in the United States and a few in Latin America, yet their headquarters are 20 minutes from our plant. Prestige Label offered an extension of their production capabilities, not duplication." According to Tropper, over the course of the past 18 months, the company had received multiple offers from both strategics and financial investors. The majority of those offers however would have meant shutting down the plant and consolidating the business with other small and mid-sized private companies, consolidating in order to drive costs out while keeping the customer base and production equipment.

Another key driver to the spike in present day merger and acquisition (M&A) activity is the renewed appeal of the packaging sector, and specifically within it, the subsectors of labeling and flexible packaging.

Louis Mitchell, Managing Director for Chicago-based Mesirow Financial, completed 14 different transactions in the packaging arena in 2005 and has completed seven so far in 2006. "I've never seen markets like this in the manufacturing sector," Mitchell states. "M&A activity is at an all time high and private equity firms like the packaging sector. They see a subsegment like labeling as being fragmented, so they see an opportunity in trying to consolidate the sector."

Mitchell and Girald hesitate to predict how much longer the boom in private equity interest in labeling will remain. But both caution that if the credit markets contract and banks become increasingly conservative, financial buyers won't be able to raise appropriate amounts of leverage and valuations will be directly impacted. In terms of the strategic investors, when the stock market declines over a certain period, they're not going to be able to use capital to acquire companies, and that could result in a potential shutting down of both avenues for label printers intent on selling.

Today, the modus operandi for any label converter interested in selling is to create as much competition as possible when positioning the company. Sure, letting the acquiring strategic investors out there know your motives is a wise move, but don't rule out what the private equity universe might be able to provide. As Girald explains, "If you're an owner of a private label company, all of your net worth might be tied up in your company. You might have paid off your mortgage, you might have some nice cars in your garage and a small portfolio, but the vast majority of your capital is tied up in your company. It's illiquid. And what a private equity firm enables a private business owner to do is to diversify his concentration. A private equity firm comes in, offers cash, and now the owner can take his capital out of the company and put it wherever he wants while still maintaining a piece of the business. The owner gets the benefit of being able to still grow the company and someday that private equity firm is going to need to sell the business to get their own return, and at that time the owner gets a second bite of the apple."

A piece of advice to business owners: Don't hang up the phone when contacted by credible investment banks, brokerages and strategics. Give them a few minutes of your time if selling is on your radar screen within the next half decade. Competition creates the best value, and exploring all of the options currently available in today's market just might present you with the opportunity of a lifetime.

One of the primary forces at work in creating the current "seller's market" scenario is the flood of private equity capital available today to invest in privately held businesses. John-Michael Girald, principal of the Bigelow Company, a New Hampshire, USA based private investment bank that has worked with label printing companies, comments on today's private equity landscape. "In our database alone we have more than 1,000 private equity firms who have each raised more than $100 million in private equity capital. If you do the math, that's around $100 billion worth of purchasing power out there today and they're investing in private companies across the country. It's a unique situation for the private company owner, because all of a sudden they have a multitude of entities wanting to bid on their business, and it is driving prices up."

Why the present private equity frenzy? Analysts claim that there are a host of explanations for this, and Girald attributes it to several key factors pervading the marketplace. "Everyone has asset allocation for their own portfolios," Girald continues, "and as the Sarbanes-Oxley Act has imposed strict accounting rules onto public companies, it makes less and less sense for small public companies to actually be public. As part of everyone's asset allocation they always invest a percentage of their money in small cap stocks, and as these stocks go away due to forces like Sarbanes-Oxley, to satisfy these small company portfolio requirements they're looking to private equity which invests in small companies in a liquid market." The graph on this page illustrates uninvested private equity capital growth over the course of the past decade.

For many label company owners, the world of private equity is an unknown. Historically, an owner considering the sale process might sit down with one of the known acquiring "strategics" — a CCL, a WS Packaging, or a Clondalkin, for example. Said owner might think his or her company is a good fit for one of these conglomerates given the company's application mix, or technology base. Some owners still view this as their best bet scenario.

Girald believes, however, that this approach is often not in the owner's best interest. "In our view, the strategic investors have their own opinion of the industry, and what we found is that the strategics often had a lower opinion of the value of a business than the private equity firms. You might get a strategic coming in with a valuation of four to five times [four to five times EBITDA] even though a company warrants a higher valuation. No matter how you try pitching this company to a group of strategics, they have a set valuation for what they pay for companies because they believe their industry experience justifies that number." The graph at right illustrates debt multiples over the course of the past decade.

Strategic investors might not want to generally boost valuation offerings, but there are some situations where a label company might be uniquely positioned to deliver its own differentiating value proposition — with RFID, for example — and in this situation a strategic investor might be willing to pay beyond the limits of the private equity universe.

Both strategic and private equity investors can deliver a scenario that is in alignment with the desires of the private company owner. Burgaw, NC, USA based Prestige Label was recently sold to Atlantic Packaging, a family owned company active in commercial and customized paper and paperboard converting. Elisha Tropper, the former president of Prestige Label, comments on his company's journey in the acquisition process.

"A priority for us was to make sure that whoever bought the company was going to keep the company in its current location and retain the employees. Atlantic was the perfect buyer. They're a large company with eight locations in the United States and a few in Latin America, yet their headquarters are 20 minutes from our plant. Prestige Label offered an extension of their production capabilities, not duplication." According to Tropper, over the course of the past 18 months, the company had received multiple offers from both strategics and financial investors. The majority of those offers however would have meant shutting down the plant and consolidating the business with other small and mid-sized private companies, consolidating in order to drive costs out while keeping the customer base and production equipment.

Another key driver to the spike in present day merger and acquisition (M&A) activity is the renewed appeal of the packaging sector, and specifically within it, the subsectors of labeling and flexible packaging.

Louis Mitchell, Managing Director for Chicago-based Mesirow Financial, completed 14 different transactions in the packaging arena in 2005 and has completed seven so far in 2006. "I've never seen markets like this in the manufacturing sector," Mitchell states. "M&A activity is at an all time high and private equity firms like the packaging sector. They see a subsegment like labeling as being fragmented, so they see an opportunity in trying to consolidate the sector."

Mitchell and Girald hesitate to predict how much longer the boom in private equity interest in labeling will remain. But both caution that if the credit markets contract and banks become increasingly conservative, financial buyers won't be able to raise appropriate amounts of leverage and valuations will be directly impacted. In terms of the strategic investors, when the stock market declines over a certain period, they're not going to be able to use capital to acquire companies, and that could result in a potential shutting down of both avenues for label printers intent on selling.

Today, the modus operandi for any label converter interested in selling is to create as much competition as possible when positioning the company. Sure, letting the acquiring strategic investors out there know your motives is a wise move, but don't rule out what the private equity universe might be able to provide. As Girald explains, "If you're an owner of a private label company, all of your net worth might be tied up in your company. You might have paid off your mortgage, you might have some nice cars in your garage and a small portfolio, but the vast majority of your capital is tied up in your company. It's illiquid. And what a private equity firm enables a private business owner to do is to diversify his concentration. A private equity firm comes in, offers cash, and now the owner can take his capital out of the company and put it wherever he wants while still maintaining a piece of the business. The owner gets the benefit of being able to still grow the company and someday that private equity firm is going to need to sell the business to get their own return, and at that time the owner gets a second bite of the apple."

A piece of advice to business owners: Don't hang up the phone when contacted by credible investment banks, brokerages and strategics. Give them a few minutes of your time if selling is on your radar screen within the next half decade. Competition creates the best value, and exploring all of the options currently available in today's market just might present you with the opportunity of a lifetime.