Jennifer Dochstader01.11.07

Latin America has notoriously been a difficult region to do business in, with a long history of cyclic economic and political extremes. The 1990s was a decade of explosive growth for the Latin American narrow web sector. As inflation rates and import tariffs on capital goods decreased throughout the region, consumer products companies strove to meet the expanding spending habits of a burgeoning middle class. Label converters in the region imported hundreds of printing presses to meet the demands of their customers' growing markets, and invested in technology as globalized print standards began to make their way onto Latin American production floors.

By the year 2000, however, the Latin American markets had cooled. Currency devaluations and political uncertainty was widespread, and the world watched as the Argentinean economy plunged. Industry suppliers to the region reported that the momentum had reached a hiatus and the slowdown in the US economy the following year further impacted regional growth percentages.

Recent years have put Latin America back on the radar screens of financial investors and industry suppliers. From 2000 to 2005, total GDP growth in the major economies was reported as follows: Brazil with 16.2 percent real growth for the period; Mexico 19.9 percent; Chile 40 percent, and Argentina 15.8 percent.* This past year once again brought government elections and political uncertainty to Latin America's two economic shining stars — Brazil and Mexico. However despite political unrest, this time around both countries demonstrated a new economic resilience as both markets persevered and the two countries further reinforced their position as growing global economic contenders.

As with any global developing economy, pressure sensitive label growth is directly tied to the expansion of the consuming classes. Consumer packaged goods manufacturers (CPGs) proliferate brands and brand line extensions as consumers become increasingly sophisticated and demand more convenient packaging with higher graphic appeal.

Over the past decade, Latin America's own packaging growth has often been overshadowed by surging rates occurring in China, India and Eastern Europe. However, Latin America was still one of the world's highest growth packaging regions from 1998 to 2005 with total consumption of packaging growing more than 14 percent. In addition to rising numbers of consumers, regional growth drivers include improved distribution networks, increasing global manufacturer consolidation and spikes in packaged food sales due to steadily increasing consumer spending power.

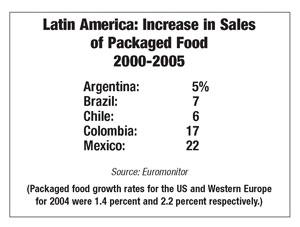

Food and beverage continue to reign as the cornerstones for Latin America's packaging growth curves and both sectors have consistently performed well above growth rates in the US and Western Europe. The table below illustrates growth percentages in sales of packaged food in the Latin American marketplace from 2000-2005.

Other forces at work in shaping Latin American consumer packaged goods company trends include European currency fluctuations, making European imports increasingly expensive. The Mercosur region in particular (Argentina, Brazil, Chile, Bolivia, and Uruguay) has historically had a loyalty to European-made products. With these goods becoming more and more expensive, local consumers have turned to high-quality local brands, driving prime label demand in these sectors.

Brazil and Mexico make up more than 60 percent of Latin America's total population, and it is in these regions that packaging and printing behemoths are investing and staking local claims in the market. Brazil alone accounts for more than 40 percent of Latin America's total packaging volume. Mexico's growth in the packaging sector has been propelled by the continued transference of US printing capacity to locations south of the border. Another key factor driving Mexico's growth is the country's per capita income level — $7,200 annually — compared with the regional average of $5,200, pushing higher levels of consumer products-acquiring consumers into the marketplace.

In one of the Latin American label printing industry's most significant moves of 2006, CCL Industries announced in January the company's acquisition of the label converting assets of Brazil based Prodesmaq, one of Brazil's largest suppliers of highest quality pressure sensitive labels. CCL then announced later in the year the company's intention of investing more than $40 million over the next two years in the company's label, container and plastic tube operations in Mexico City, tagging $9 million for label converting and prepress technologies which will include the purchase of new offset and rotogravure press systems.

Narrow to mid-web label printers in Mexico and Brazil are reporting 2006 growth rates of 15 to 20 percent. Jeffrey Arippol, owner and president of Novelprint, a prominent label printing company based in São Paulo, Brazil, comments on factors driving the industry in his region. "In Brazil, you have this large mass of population that was never a consuming universe, and suddenly their incomes are rising and they're in the market as consumers. This is one of the primary reasons growth is so high. Additionally, other consumer products companies have entered the market and are becoming competitive against multinationals like Procter & Gamble and Unilever." Increased market presence from these second-tier companies, or 'B brands', is frequently cited as one of Latin America's packaging megatrends, driving growth across consumer products packaging sectors.

CCL's strategic initiatives in Latin America reinforce the fact that highest level globalized print standards are in the region to stay, and that the region's supermarket and pharmacy shelves are increasingly going to be stocked with products yielding world class graphic aesthetics. Arippol comments on the pressures of meeting heightening globalized print standards. "Global standard procedures are more and more in effect. For example, the Unilever labels produced in Brazil have to be exactly the same as those produced in Chile, Argentina, the US, and Europe. We have invested in gravure printing press systems because companies like Unilever are saying, 'We don't want UV flexo. We want either offset or gravure.' In the past year Brazil has been really hit by global procedures. In January, CCL acquired Prodesmaq and in August another multi-conglomerate purchased Pimaco, a label printing company in Rio de Janeiro. All of a sudden we have multinational competitors and it's a major turning point for this market."

Industry suppliers to the Latin American region have had a good year as press export volumes are up and consumable and press auxiliary equipment suppliers are reporting business has spiked in the region as well. Mike Russell, international sales manager for Mark Andy, says he is seeing sales come from a variety of countries in the region, not just the heavyweights Brazil and Mexico. "This has been a very good year for Mark Andy in Latin America. Our sales are up in the region 20 to 30 percent over last year, and it's a good balance among countries throughout the region, it's not concentrated in one country. We did well in Mexico and Brazil but also saw sales increase in Venezuela, Colombia, Chile, and Panama."

Asked about the sophistication level of the press systems Mark Andy is selling in the region, Russell indicates that he's seeing a technology shift in the machines sold. "A lot of these presses are going out UV flexo, and some are going out set up for shrink sleeves. I'm seeing a shift in Latin America away from water based toward UV flexo.

"As far as the future, I think Brazil is going to be the most promising market, especially for higher end presses," says Russell. "In Brazil, you have a local press manufacturer so in that market we're going to be concentrating on more sophisticated applications. We recently sold an XP 5000 into Brazil, a servo press that is going to be installed in 2007. This is a top of the line press, and I think this will be a trend that will increase for us in Brazil."

Press manufacturer Gallus has also witnessed an increase in momentum in these markets and has recently hired Hans-Ramón Hofmann as regional sales director for the region, working out of Mexico City. Hofmann sees his new role as a welcome challenge. "The vast majority of the market here is water based," he explains. "That's one of the reasons I took this challenge because I think that's going to change and evolve as consumers obtain more and more purchasing power."

Hofmann says that a high volume of prime labels are still being imported into Mexico from the US and Europe, but that this can be looked at as an additional opportunity for Mexican label printers. "Mexican end users are still looking outside Mexico for some of the highest quality printed labels. Why? This is difficult to answer. Part of the reason is due to a type of psychology that Mexican companies have, and that is that Mexican products aren't as good as those coming from the United States and Europe. I believe that the other part is due to a general lack of knowledge in the industry — that we have the necessary production technology in the country, and are capable of printing these applications at the same quality levels as the United States and Europe."

For decades, label printers and industry suppliers have rode out boom-and-bust cycles in the Latin American region. And as manufacturers today focus much of their developmental efforts on another hemisphere where hot markets like India, China and Russia hold the promise of double-digit growth and profits, suppliers shouldn't forget about our continental neighbor to the south where thriving consuming classes will continue to push label demand beyond the annual growth rates occurring in their own backyards.

By the year 2000, however, the Latin American markets had cooled. Currency devaluations and political uncertainty was widespread, and the world watched as the Argentinean economy plunged. Industry suppliers to the region reported that the momentum had reached a hiatus and the slowdown in the US economy the following year further impacted regional growth percentages.

Recent years have put Latin America back on the radar screens of financial investors and industry suppliers. From 2000 to 2005, total GDP growth in the major economies was reported as follows: Brazil with 16.2 percent real growth for the period; Mexico 19.9 percent; Chile 40 percent, and Argentina 15.8 percent.* This past year once again brought government elections and political uncertainty to Latin America's two economic shining stars — Brazil and Mexico. However despite political unrest, this time around both countries demonstrated a new economic resilience as both markets persevered and the two countries further reinforced their position as growing global economic contenders.

A growing consumer class fuels label growth

As with any global developing economy, pressure sensitive label growth is directly tied to the expansion of the consuming classes. Consumer packaged goods manufacturers (CPGs) proliferate brands and brand line extensions as consumers become increasingly sophisticated and demand more convenient packaging with higher graphic appeal.

Over the past decade, Latin America's own packaging growth has often been overshadowed by surging rates occurring in China, India and Eastern Europe. However, Latin America was still one of the world's highest growth packaging regions from 1998 to 2005 with total consumption of packaging growing more than 14 percent. In addition to rising numbers of consumers, regional growth drivers include improved distribution networks, increasing global manufacturer consolidation and spikes in packaged food sales due to steadily increasing consumer spending power.

Food and beverage continue to reign as the cornerstones for Latin America's packaging growth curves and both sectors have consistently performed well above growth rates in the US and Western Europe. The table below illustrates growth percentages in sales of packaged food in the Latin American marketplace from 2000-2005.

Other forces at work in shaping Latin American consumer packaged goods company trends include European currency fluctuations, making European imports increasingly expensive. The Mercosur region in particular (Argentina, Brazil, Chile, Bolivia, and Uruguay) has historically had a loyalty to European-made products. With these goods becoming more and more expensive, local consumers have turned to high-quality local brands, driving prime label demand in these sectors.

Regional superstars: Brazil and Mexico

Brazil and Mexico make up more than 60 percent of Latin America's total population, and it is in these regions that packaging and printing behemoths are investing and staking local claims in the market. Brazil alone accounts for more than 40 percent of Latin America's total packaging volume. Mexico's growth in the packaging sector has been propelled by the continued transference of US printing capacity to locations south of the border. Another key factor driving Mexico's growth is the country's per capita income level — $7,200 annually — compared with the regional average of $5,200, pushing higher levels of consumer products-acquiring consumers into the marketplace.

In one of the Latin American label printing industry's most significant moves of 2006, CCL Industries announced in January the company's acquisition of the label converting assets of Brazil based Prodesmaq, one of Brazil's largest suppliers of highest quality pressure sensitive labels. CCL then announced later in the year the company's intention of investing more than $40 million over the next two years in the company's label, container and plastic tube operations in Mexico City, tagging $9 million for label converting and prepress technologies which will include the purchase of new offset and rotogravure press systems.

Narrow to mid-web label printers in Mexico and Brazil are reporting 2006 growth rates of 15 to 20 percent. Jeffrey Arippol, owner and president of Novelprint, a prominent label printing company based in São Paulo, Brazil, comments on factors driving the industry in his region. "In Brazil, you have this large mass of population that was never a consuming universe, and suddenly their incomes are rising and they're in the market as consumers. This is one of the primary reasons growth is so high. Additionally, other consumer products companies have entered the market and are becoming competitive against multinationals like Procter & Gamble and Unilever." Increased market presence from these second-tier companies, or 'B brands', is frequently cited as one of Latin America's packaging megatrends, driving growth across consumer products packaging sectors.

CCL's strategic initiatives in Latin America reinforce the fact that highest level globalized print standards are in the region to stay, and that the region's supermarket and pharmacy shelves are increasingly going to be stocked with products yielding world class graphic aesthetics. Arippol comments on the pressures of meeting heightening globalized print standards. "Global standard procedures are more and more in effect. For example, the Unilever labels produced in Brazil have to be exactly the same as those produced in Chile, Argentina, the US, and Europe. We have invested in gravure printing press systems because companies like Unilever are saying, 'We don't want UV flexo. We want either offset or gravure.' In the past year Brazil has been really hit by global procedures. In January, CCL acquired Prodesmaq and in August another multi-conglomerate purchased Pimaco, a label printing company in Rio de Janeiro. All of a sudden we have multinational competitors and it's a major turning point for this market."

Opportunities for suppliers

Industry suppliers to the Latin American region have had a good year as press export volumes are up and consumable and press auxiliary equipment suppliers are reporting business has spiked in the region as well. Mike Russell, international sales manager for Mark Andy, says he is seeing sales come from a variety of countries in the region, not just the heavyweights Brazil and Mexico. "This has been a very good year for Mark Andy in Latin America. Our sales are up in the region 20 to 30 percent over last year, and it's a good balance among countries throughout the region, it's not concentrated in one country. We did well in Mexico and Brazil but also saw sales increase in Venezuela, Colombia, Chile, and Panama."

Asked about the sophistication level of the press systems Mark Andy is selling in the region, Russell indicates that he's seeing a technology shift in the machines sold. "A lot of these presses are going out UV flexo, and some are going out set up for shrink sleeves. I'm seeing a shift in Latin America away from water based toward UV flexo.

"As far as the future, I think Brazil is going to be the most promising market, especially for higher end presses," says Russell. "In Brazil, you have a local press manufacturer so in that market we're going to be concentrating on more sophisticated applications. We recently sold an XP 5000 into Brazil, a servo press that is going to be installed in 2007. This is a top of the line press, and I think this will be a trend that will increase for us in Brazil."

Press manufacturer Gallus has also witnessed an increase in momentum in these markets and has recently hired Hans-Ramón Hofmann as regional sales director for the region, working out of Mexico City. Hofmann sees his new role as a welcome challenge. "The vast majority of the market here is water based," he explains. "That's one of the reasons I took this challenge because I think that's going to change and evolve as consumers obtain more and more purchasing power."

Hofmann says that a high volume of prime labels are still being imported into Mexico from the US and Europe, but that this can be looked at as an additional opportunity for Mexican label printers. "Mexican end users are still looking outside Mexico for some of the highest quality printed labels. Why? This is difficult to answer. Part of the reason is due to a type of psychology that Mexican companies have, and that is that Mexican products aren't as good as those coming from the United States and Europe. I believe that the other part is due to a general lack of knowledge in the industry — that we have the necessary production technology in the country, and are capable of printing these applications at the same quality levels as the United States and Europe."

For decades, label printers and industry suppliers have rode out boom-and-bust cycles in the Latin American region. And as manufacturers today focus much of their developmental efforts on another hemisphere where hot markets like India, China and Russia hold the promise of double-digit growth and profits, suppliers shouldn't forget about our continental neighbor to the south where thriving consuming classes will continue to push label demand beyond the annual growth rates occurring in their own backyards.